WORLD PROGRESS TOWARD SOUND MONEY IN 1926-27

TWO interesting statements, at first glance more contradictory than they appear to be upon closer analysis, are made by commentators on currency rehabilitation in Europe.

It is stated in a bulletin from the Stock Exchange house of Dominick and Dominick that looking back on the events of 1926 it is evident that "the condition of international exchange to-day is better than at any time in the past six years," and that the general "monetary stabilization and balancing of the budget throughout the world" are extremely encouraging. Looking ahead the New York Journal of Commerce sees a large part of Europe "still facing the supreme final effort that is required before budgets can be safely regarded as balanced and currencies confidently considered to be stabilized." The first observer is thinking of the progress that has been made, the second of what is still to be achieved. Let us consider for a moment the facts noted by the New York brokerage house. It reminds us that:

France and Italy now remain the only two important countries where currency stabilization has not been accomplished. The world movement toward a return to the gold standard, begun in 1922, is practically completed. Since Great Britain adopted the gold basis in the spring of 1925, eleven countries have followed in its foot-steps.

For most countries, the adoption of the gold standard has assumed a modified form. As a rule, gold was not put into circulation, and its export and import movement was regulated. Of the eleven European countries which have returned to the gold standard since the war, only two of them Finland and Great Britainhave a note issue convertible into gold; and none of them has gold in circulation.

The drastic monetary reform in Belgium was the most important financial achievement of the year just ended. At the beginning of the year the Belgian franc was valued at about four and one-half cents, but efforts to stabilize it at that point failed, and it dropt to a little over two cents. With the aid of an international loan of $100,000,000, a new unitthe belgawas introduced on the gold basis, equal to five of the old francs. The change seems to be successful and permanent.

There is no unanswerable reason why the same policy should not be followed in Italy and France.

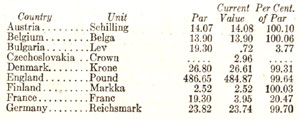

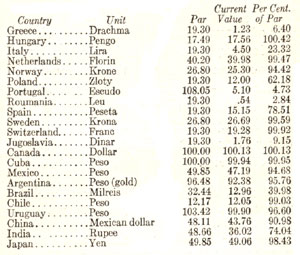

The following table is then presented showing the approximate present value in cents, as compared with the par value, of the currency units of the principal nations of the world:

Ten countries, according to this table, are using a currency unit which is far below its par value. The writer for the New York brokerage firm points out that besides France and Italy, Portugal, Bulgaria, Czechoslovakia, Greece, Jugoslavia and Roumania have successfully maintained their currency at an even level and are likely to stabilize it on the gold basis at that level. It is noted that:

Poland has been the one country establishing a new unit which has failed to maintain its value. Under the leadership of Dr. Kemmerer, the monetary system has been reorganized again this year and is improving. And Brazil, the last of the ten, is considering the stabilization of the milreis at its current figure of about twelve cents.

In the countries not yet on a gold basis, therefore, stabilization is approximately achieved. The condition of international exchange to-day is better than at any time in the past six years.

But there is still much to be done, the New York Journal of Commerce insists. Outside pressure compelled Germany to reform, "but in the ease of her neighbors, lack of external compulsion has made it very difficult to overcome the internal political obstacles that are always encountered by Governments confronted with hard tasks and financial rehabilitation." All honest efforts to stabilize currency bring their trials and tribulations. So it is held to be very probable "that 1927 will prove to be a year which will provide severe tests of the good faith and determination of Europe to fulfil promises that have been previously made":

The months ahead may prove to be a period of rather painful probation for many countries. They will certainly bring losses and costly readjustments to industry. Taxes will be heavy and can not be escaped as heretofore by the gateway of inflation. Export premiums will disappear as currencies are stabilized, orders will fail, unemployment will increase, and demands upon Governments consequently will grow as revenues tend to diminish.

Belgium is already tasting the after-effects of stabilization, France is sampling it in advance, and Italy is doing likewise. If the governing authorities of these three countries are prepared to insist upon the relentless execution of financial reform measures, the year 1927 will end with the greater part of Europe reestablished upon a solid, stable, peace-time basis that will make it possible to take stock of the future, to develop international trade by negotiating definitive commercial treaties and to fix taxes and import duties on the basis of predictable price-levels and dependable exchanges.

Source: The Literary Digest for February 5, 1927

It is stated in a bulletin from the Stock Exchange house of Dominick and Dominick that looking back on the events of 1926 it is evident that "the condition of international exchange to-day is better than at any time in the past six years," and that the general "monetary stabilization and balancing of the budget throughout the world" are extremely encouraging. Looking ahead the New York Journal of Commerce sees a large part of Europe "still facing the supreme final effort that is required before budgets can be safely regarded as balanced and currencies confidently considered to be stabilized." The first observer is thinking of the progress that has been made, the second of what is still to be achieved. Let us consider for a moment the facts noted by the New York brokerage house. It reminds us that:

France and Italy now remain the only two important countries where currency stabilization has not been accomplished. The world movement toward a return to the gold standard, begun in 1922, is practically completed. Since Great Britain adopted the gold basis in the spring of 1925, eleven countries have followed in its foot-steps.

For most countries, the adoption of the gold standard has assumed a modified form. As a rule, gold was not put into circulation, and its export and import movement was regulated. Of the eleven European countries which have returned to the gold standard since the war, only two of them Finland and Great Britainhave a note issue convertible into gold; and none of them has gold in circulation.

The drastic monetary reform in Belgium was the most important financial achievement of the year just ended. At the beginning of the year the Belgian franc was valued at about four and one-half cents, but efforts to stabilize it at that point failed, and it dropt to a little over two cents. With the aid of an international loan of $100,000,000, a new unitthe belgawas introduced on the gold basis, equal to five of the old francs. The change seems to be successful and permanent.

There is no unanswerable reason why the same policy should not be followed in Italy and France.

The following table is then presented showing the approximate present value in cents, as compared with the par value, of the currency units of the principal nations of the world:

Ten countries, according to this table, are using a currency unit which is far below its par value. The writer for the New York brokerage firm points out that besides France and Italy, Portugal, Bulgaria, Czechoslovakia, Greece, Jugoslavia and Roumania have successfully maintained their currency at an even level and are likely to stabilize it on the gold basis at that level. It is noted that:

Poland has been the one country establishing a new unit which has failed to maintain its value. Under the leadership of Dr. Kemmerer, the monetary system has been reorganized again this year and is improving. And Brazil, the last of the ten, is considering the stabilization of the milreis at its current figure of about twelve cents.

In the countries not yet on a gold basis, therefore, stabilization is approximately achieved. The condition of international exchange to-day is better than at any time in the past six years.

But there is still much to be done, the New York Journal of Commerce insists. Outside pressure compelled Germany to reform, "but in the ease of her neighbors, lack of external compulsion has made it very difficult to overcome the internal political obstacles that are always encountered by Governments confronted with hard tasks and financial rehabilitation." All honest efforts to stabilize currency bring their trials and tribulations. So it is held to be very probable "that 1927 will prove to be a year which will provide severe tests of the good faith and determination of Europe to fulfil promises that have been previously made":

The months ahead may prove to be a period of rather painful probation for many countries. They will certainly bring losses and costly readjustments to industry. Taxes will be heavy and can not be escaped as heretofore by the gateway of inflation. Export premiums will disappear as currencies are stabilized, orders will fail, unemployment will increase, and demands upon Governments consequently will grow as revenues tend to diminish.

Belgium is already tasting the after-effects of stabilization, France is sampling it in advance, and Italy is doing likewise. If the governing authorities of these three countries are prepared to insist upon the relentless execution of financial reform measures, the year 1927 will end with the greater part of Europe reestablished upon a solid, stable, peace-time basis that will make it possible to take stock of the future, to develop international trade by negotiating definitive commercial treaties and to fix taxes and import duties on the basis of predictable price-levels and dependable exchanges.

Source: The Literary Digest for February 5, 1927